If you're trying to sell a house in pre-foreclosure in Martin County, FL, you're probably dealing with a lot of stress and not a lot of clear answers. The good news is that pre-foreclosure is not the end of the road. It's actually a window — one that gives you time to act, protect your credit, and walk away with more control than most homeowners realize.

This guide walks through what pre-foreclosure means in Martin County, what your real options are, and how the process works step by step.

What Pre-Foreclosure Actually Means in Florida

Pre-foreclosure begins when your lender files a lis pendens (a notice of pending legal action) with the Martin County Clerk of Court. This is the formal start of the foreclosure process in Florida, which is judicial — meaning it goes through the courts.

Once that filing happens, you typically have a period of several months before a final judgment and auction date are set. During this window, you still own the home. You still have the legal right to sell it.

That distinction matters. Many homeowners along the Treasure Coast — in neighborhoods from Palm City to Port Salerno to Indiantown — assume that once they receive a foreclosure notice, it's too late. It usually isn't.

Why Selling Before Foreclosure Is Worth Considering

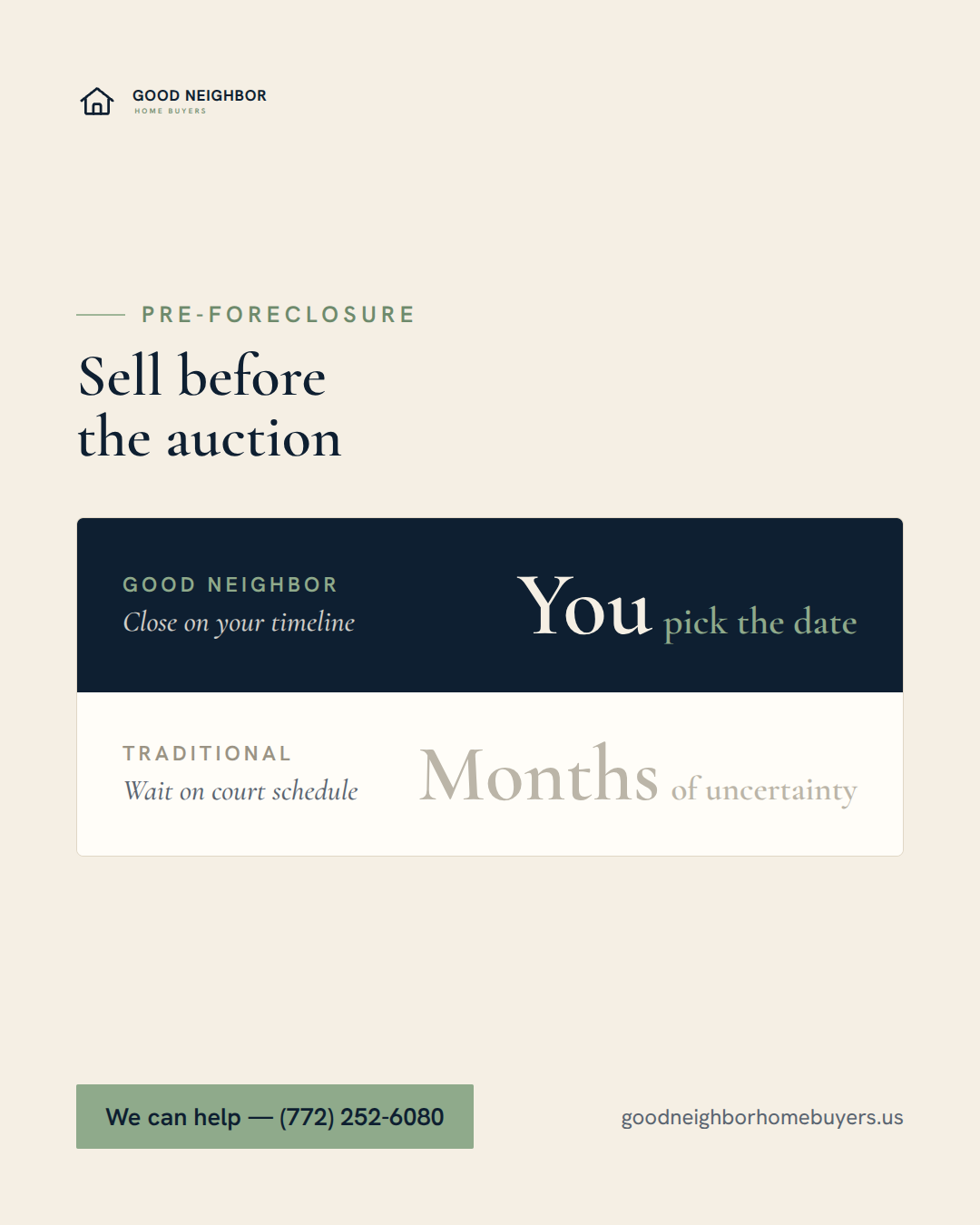

A completed foreclosure stays on your credit report for up to seven years and can make it difficult to buy another home, rent in certain communities, or even qualify for some jobs. Selling before that happens can soften the blow significantly.

When you sell during pre-foreclosure, you may be able to pay off your mortgage balance, avoid a deficiency judgment, and keep the process out of the public record as a completed foreclosure. If there's equity in the home, you may walk away with cash in hand.

Even if you owe more than the home is worth, a short sale — where the lender agrees to accept less than the full balance — may still be an option. It's not simple, but it's far better than the alternative for most people.

Sell House Pre-Foreclosure Martin County FL: Your Realistic Options

Here's an honest look at the paths available to you right now:

1. List with a real estate agent. This can work if you have enough time before the court date and the home is in good condition. Keep in mind that agent commissions, closing costs, and the time needed for showings and buyer financing can eat into both your timeline and your proceeds.

2. Sell directly to a cash buyer. A direct sale to a company like Good Neighbor Home Buyers in Stuart can move much faster — often in as little as two to three weeks. There are no commissions, no repairs required, and no waiting on a buyer's mortgage approval. This is often the most practical route when the foreclosure clock is ticking.

3. Negotiate with your lender. Loan modification, forbearance, or a repayment plan may buy you time. These aren't guaranteed, but they're worth exploring — especially early in the process. You can learn more about lender negotiation and other strategies on our stop foreclosure in Florida page.

How the Timeline Works in Martin County

Florida's judicial foreclosure process is slower than in many states, which works in your favor. From the initial lis pendens filing to a scheduled sale, the process in Martin County often takes several months — sometimes longer if the court docket is busy or if the lender is slow to move.

That said, waiting too long narrows your options. The earlier you start exploring a sale, the more leverage you have. Once a sale date is set by the court, the timeline becomes much tighter.

What a Cash Sale Looks Like, Step by Step

If you're considering a direct cash sale, here's what the process typically involves:

You reach out and share some basic details about the property — its location, condition, and your situation. We review everything and, if it's a fit, present a no-obligation cash offer. There's no pressure and no commitment at that stage.

If you accept, we work with a local Martin County title company to handle the closing. You choose the date. We buy the home as-is — no cleaning, no repairs, no staging. You can see the full breakdown on our how it works page.

The goal is simple: help you close before the foreclosure is finalized, so you can move forward on your terms.

A Few Things to Keep in Mind

We're a cash home buyer, not attorneys or financial advisors. If you're in pre-foreclosure, it's wise to consult with a HUD-approved housing counselor or a Florida real estate attorney who can review your specific situation. The decisions you make now have long-term consequences, and you deserve clear, professional guidance.

We also want to be upfront: we can't guarantee a specific offer amount or outcome. Every property and situation is different. What we can offer is a straightforward, honest process with no fees and no obligation.

Frequently Asked Questions

Can I sell my house in pre-foreclosure if I owe more than it's worth?

Potentially, yes. This is called a short sale, and it requires your lender's approval. The lender agrees to accept less than the remaining mortgage balance. It takes longer than a standard sale, but it may still be possible depending on your timeline and lender.

How quickly can I close on a cash sale in Martin County?

In many cases, a cash sale can close in as little as two to three weeks. The exact timeline depends on title work and your specific situation, but it's significantly faster than a traditional listing.

Will selling in pre-foreclosure hurt my credit?

Late mortgage payments will already have affected your credit. However, selling before a completed foreclosure generally results in less long-term damage than letting the foreclosure go through. A foreclosure judgment can remain on your credit report for up to seven years.

Do I need to make repairs before selling to a cash buyer?

No. Good Neighbor Home Buyers purchases homes as-is. Whether the property needs a new roof, has code violations, or just hasn't been maintained — we handle all of that after closing.

If you're facing pre-foreclosure in Stuart or anywhere in Martin County, we're here to talk through your options — no pressure, no obligation. Call us at (772) 252-6080 or request a no-obligation cash offer whenever you're ready.

This article is general information, not legal or financial advice. For your specific situation, talk to a qualified professional.